Absense of Projections for Debts and Deficits

Extremely Optimistic Economic Assumptions

Focus on Discretionary Spending

Calculation of Projections for Debts and Deficits

Absense of Projections for Debts and Deficits

On April 3, 2026, the White House released the Fiscal Year (FY) 2027 budget, containing the administration's budget priorities and proposals for the fiscal year that begins in October. The same day, the Committee for a Responsible Federal Budget released an analysis of it on their blog titled An Overview of the President's FY 2027 Budget. The analysis begins:

The Trump Administration released its Fiscal Year (FY) 2027 budget request today. While the President's budget typically presents a comprehensive plan for addressing discretionary spending, mandatory spending, and revenue for the next decade, this year's budget includes mainly a discretionary spending request and assumptions about how the economy will grow over that period.

In a section titled "Debt and Deficits Under the President's Budget", the analysis goes on to state:

The budget presents no summary figures for debt or deficits; instead, it provides a summary of its discretionary spending request alongside a reconciliation request for further defense funding. However, the various tables in the Analytical Perspectives section allow us to impute debt, deficits, spending, and revenue in both the Office of Management and Budget's (OMB) baseline and the President's budget. We find that the budget assumes debt held by the public would grow from 100% of GDP in FY 2025 to a peak of 103% of GDP by 2029 before falling to 94% by 2036.

This highlights a very curious fact about this budget. It appears that this budget and Trump's prior budget for fiscal year 2026 may be the only budgets since at least 1977 to not include projections of the debt and deficit in future years. When asked "For how long has the Budget of the United States contained projections of the debt and deficit in the Summary and Historical Tables?", ChatGPT's reply included the following:

The Budget of the United States has contained projections of deficits and debt in its Summary and Historical Tables for essentially the entire modern budget period-about five decades since the mid-1970s.

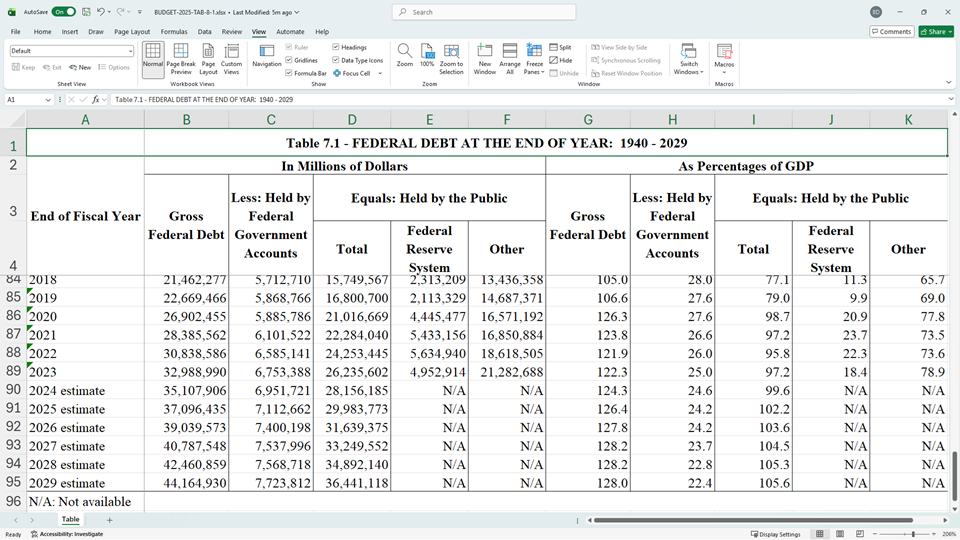

I have verified this in copies of the budget back through all those submitted by Obama. As an example of projections of the debt, following are screenshots from the relevant historical and summary tables from Biden's last budget for fiscal year 2025:

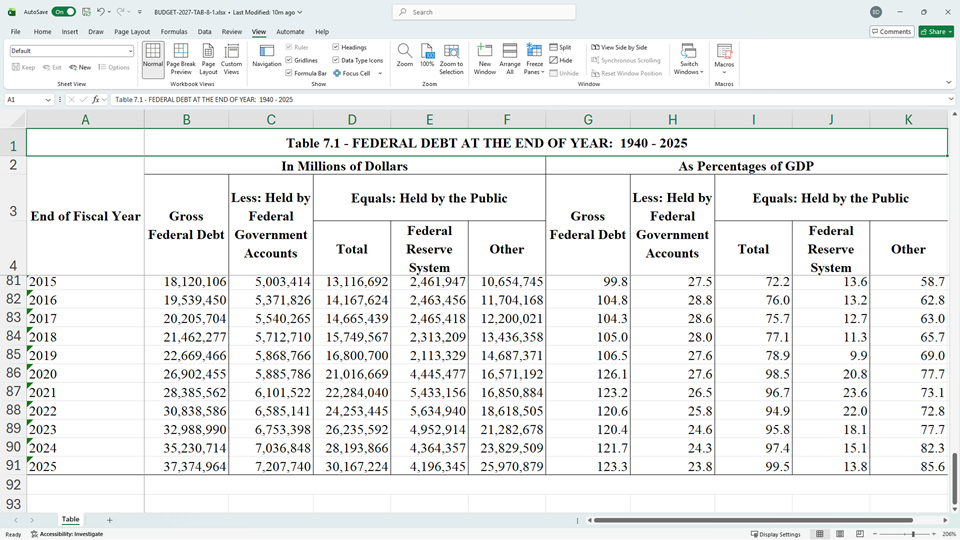

Following is a screenshot from the corresponding historical table from Trump's recent budget. That budget contained no summary table containing past or current debts, much less projected debts.

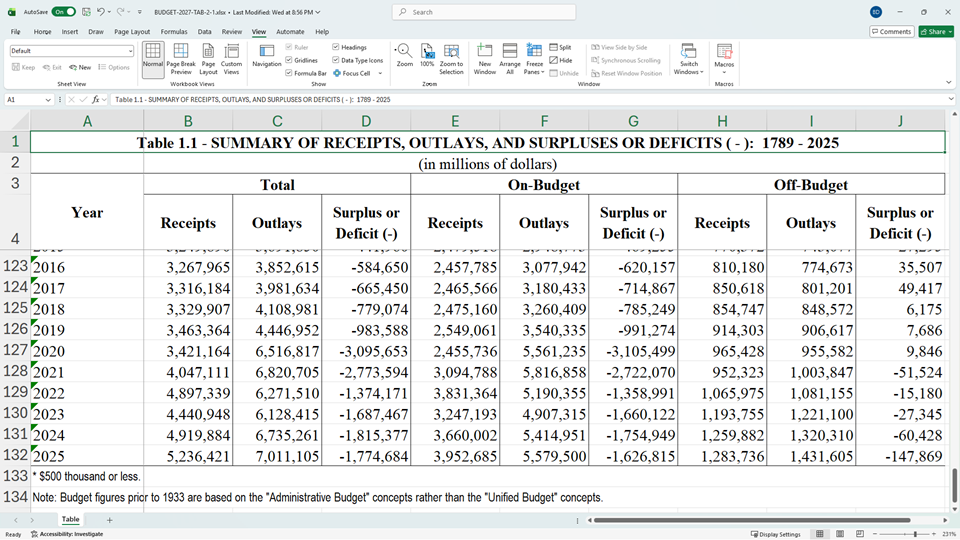

As can be seen, it contains no projections of federal debt. In addition, Table 1.1 in Trump's recent budget does not show projections of the deficit as can be seen below:

This is especially odd because Table 2.1 has projections of receipts from 2026 through 2031 and receipts before 2026 that exactly match those in the table above. Similarly, Table 3.1 has projections of outlays from 2026 through 2031 and outlays before 2026 that exactly match those shown above. From the table above, it can be seen that the deficit is simply equal to receipts minus outlays. Hence, it should have been trivial to include the projections for receipts from Table 2.1 and projections for outlays from Table 3.1 and compute the resulting projected deficits in Table 1.1 above.

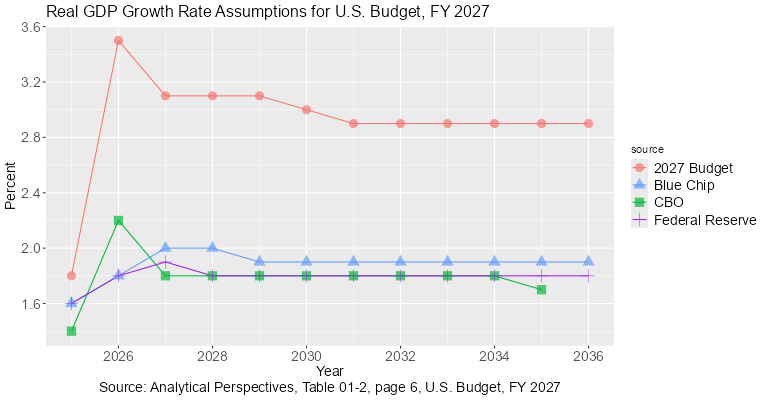

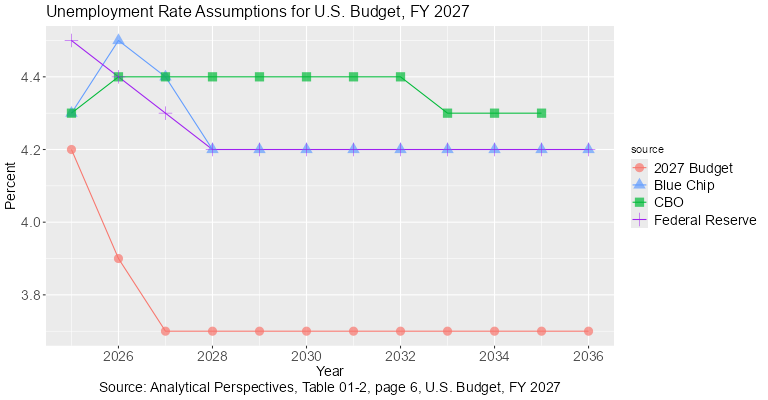

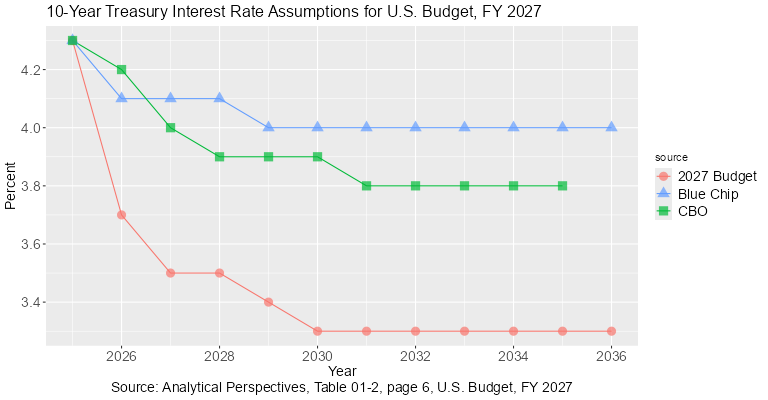

Extremely Optimistic Economic Assumptions

In a section titled "Economic Assumptions in the President's Budget", the CRFB analysis begins as follows:

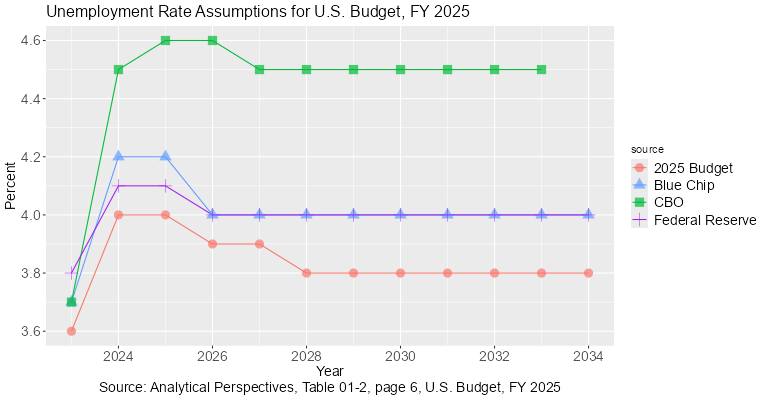

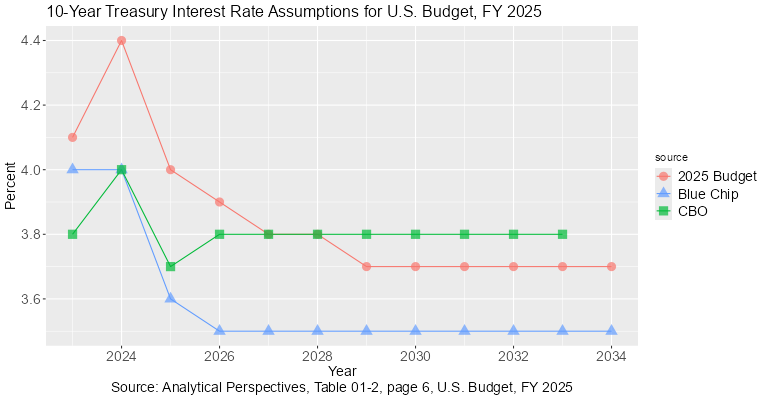

Outside of the budgetary estimates, the President's budget includes a ten-year economic forecast that is significantly more optimistic about the economy than other mainstream forecasters, such as CBO and the Federal Reserve.

The following plots show a comparison of these assumptions for real GDP growth, unemployment, and the 10-year Treasury interest rate for the next 10 years:

As can be seen, the budget projects real GDP growth to be nearly a full percentage greater than the CBO, Federal Reserve, and Blue Chip Economic Indidcators. Also, it projects the unemployment rate and the 10-year Treasury interest rate to be about half of a percent less than those sources.

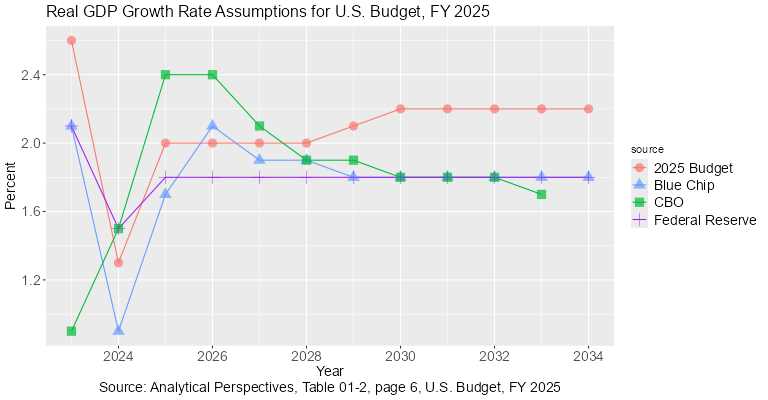

In contrast, the following plots show a comparison of these same assumptions from Biden's last budget for fiscal year 2025:

As can be seen, these assumptions are much closer to the projections of other major forecasters. The only noticable exception is unemployment where the Biden budget assumes a 0.1 to 0.2 lower unemployment rate than the Federal Reserve and Blue Chip assumptions and a 0.5 to 0.7 lower unemployment rate than the CBO assumptions.

All of the economic assumptions from the fiscal year 2025 and 2027 budgets can be viewed via the R Shiny app at https://econdata.shinyapps.io/assump1/.

Focus on Discretionary Spending

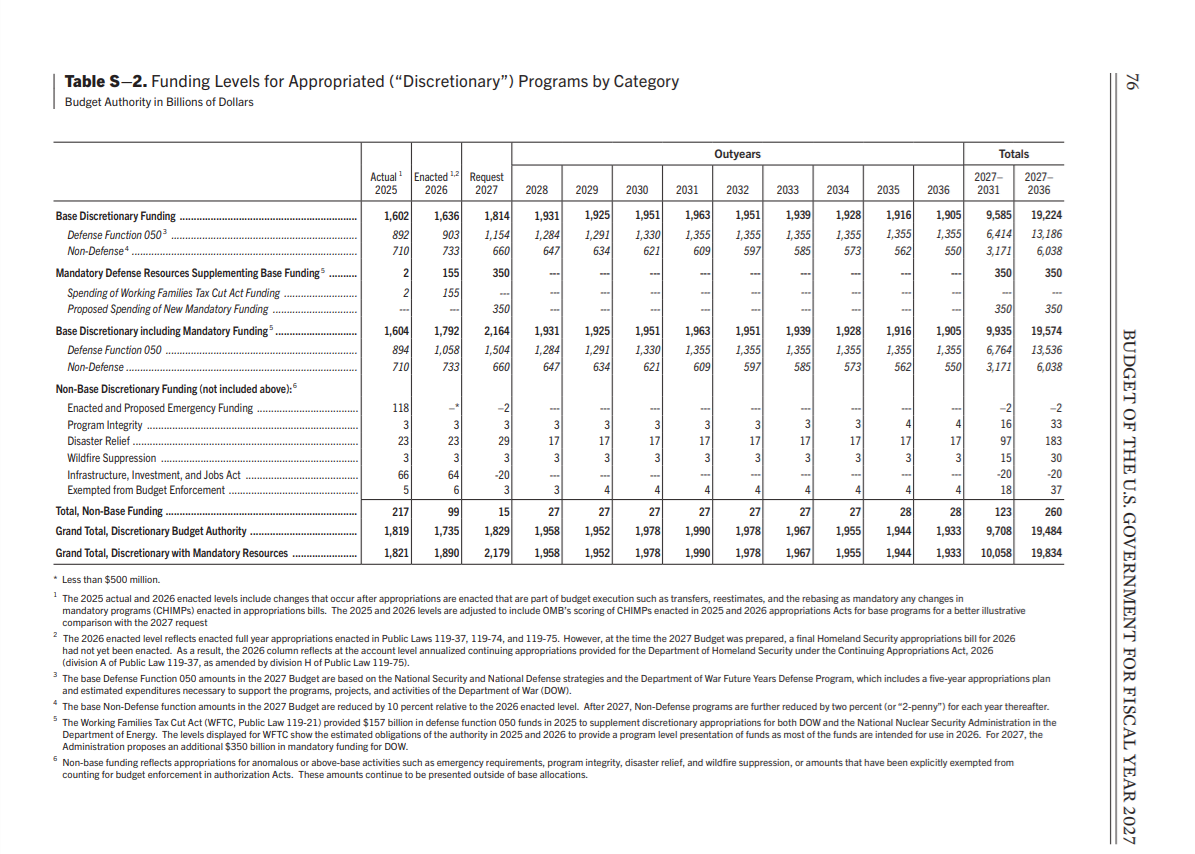

As previously mentioned, the CRFB analysis states that "this year's budget includes mainly a discretionary spending request and assumptions about how the economy will grow over that period". Following is Summary Table S-2 which shows the discretionary spending request and the projected levels of discretionary spending through 2036:

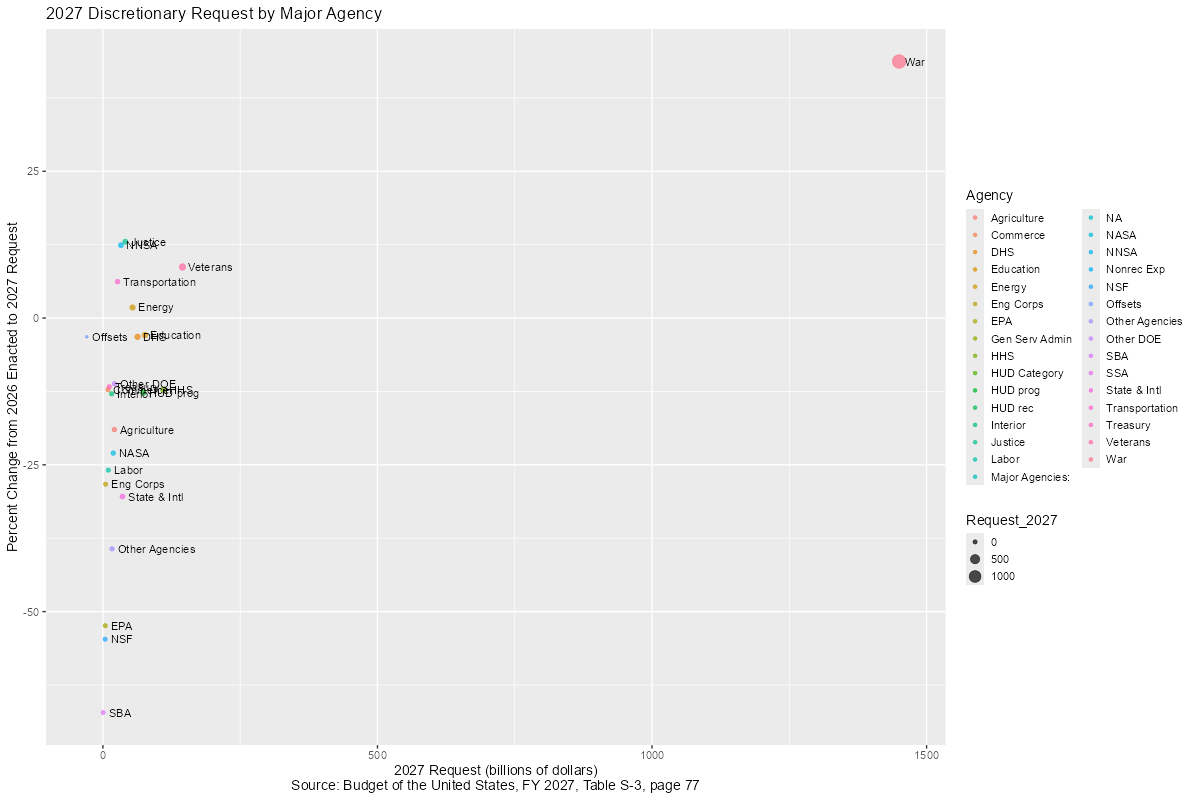

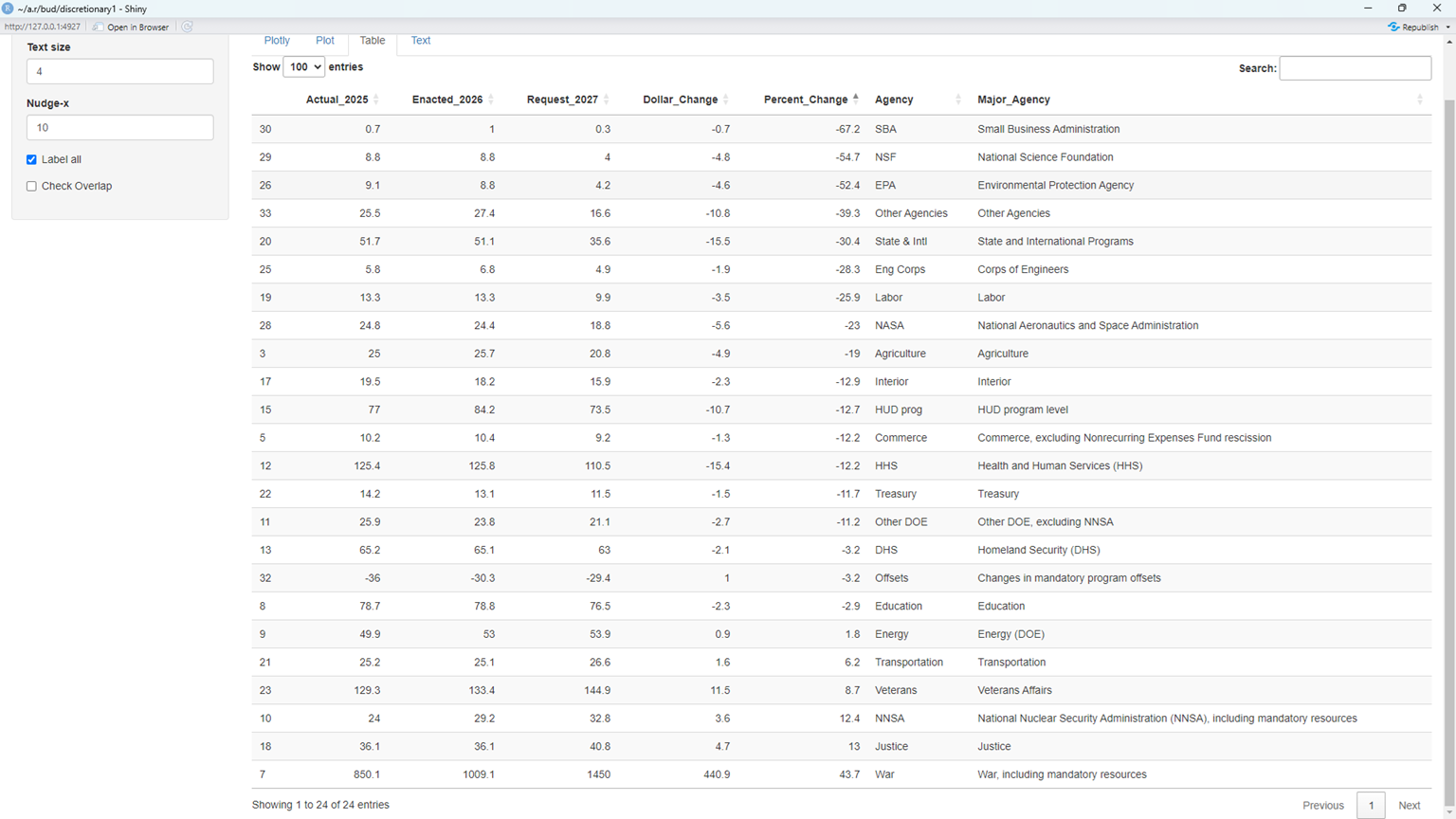

The following plot and table show the discretionary spending request for 2027 and it's percent change from the spending enacted in 2026:

An interactive version of this plot and table can be found in the R Shiny app at https://econdata.shinyapps.io/discretionary1/.

As can be seen, the request for the War Department was by far the largest at $1.45 trillion. It also had the largest increase of 43.7 percent. In addition, there were increases in Justice of 13%, National Nuclear Security Administration (NNSA) of 12.4%, Veteran's Affairs of 8.7%, Transportation of 6.2%, and Energy of 1,8%. The largest percentage decreases were to the Small Business Adminstration (SBA) of -67.2%, National Science Foundation (NSF) of 54.7%, Environmental Protection Agency of 52.4%, State and International Programs of 30.4%, the Corps of Engineers of 28.3%, Labor of 25.9%, and NASA of 23%.

Regarding these requested cuts, an analysis in the New York Times titled Trump Budget Does Little to Address Nation's Fiscal Challenges stated the following:

What the White House presented as its fiscal outlook relied on spending cuts that would be difficult to get through Congress and projections of strong government revenue, fueled by tariffs and bounding economic growth.

Calculation of Projections for Debts and Deficits

The previously mentioned New York Times analysis included the following quote:

"It's the most number-free budget we've seen in recent history," said Maya MacGuineas, the president of the bipartisan Committee for a Responsible Federal Budget. "I have to imagine that there's a story that the numbers would tell that they don't want to tell."

In addition, the prviously mentioned analysis from the Committee for a Responsible Federal Budget stated the following:

The budget presents no summary figures for debt or deficits; instead, it provides a summary of its discretionary spending request alongside a reconciliation request for further defense funding. However, the various tables in the Analytical Perspectives section allow us to impute debt, deficits, spending, and revenue in both the Office of Management and Budget's (OMB) baseline and the President's budget.

The following table lists a number of projections that can be found in the Analytical Perspectives and Historical Tables of the budget than can be used to impute those items:

RECEIPTS, OUTLAYS, SURPLUS / DEFICIT (-), DEBT from the BUDGET OF THE UNITED STATES, FISCAL YEAR 2027

Year 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 Source

HT1 Receipts 5.2364 HT: Table 1.1

HT Receipts 5.2364 5.4757 5.9210 6.2884 6.6603 7.1373 7.5594 HT: Table 2.1

AP8 Receipts 5.2364 5.4757 5.9210 6.2884 6.6603 7.1373 7.5594 7.9843 8.4468 8.8913 9.3608 9.8461 AP: Table 08-1, page 73

AP Receipts 5.2364 5.4757 5.9210 6.2884 6.6603 7.1373 7.5594 7.9843 8.4468 8.8913 9.3608 9.8461 AP: Table 12-4, page 134

HT1 Outlays 7.0111 HT: Table 1.1

HT Outlays 7.0111 7.5404 8.0929 8.4454 8.6532 8.9963 9.2798 HT: Table 3.1

AP Outlays 7.0110 7.5410 7.9450 8.2860 8.5450 8.9420 9.2650 9.6960 10.2840 10.5990 10.9040 11.5290 AP: Table 12-1, page 131

HT1 Deficit -1.7747 HT: Table 1.1

HT Deficit -1.7747 -2.0647 -2.1719 -2.1570 -1.9929 -1.8590 -1.7204 HT: Tables 2.1, 3.1 calculated

AP Deficit -1.7746 -2.0653 -2.0240 -1.9976 -1.8847 -1.8047 -1.7056 -1.7117 -1.8372 -1.7077 -1.5432 -1.6829 HT: Tables 12-1, 12-4 calculated

HT Debt Held by the Public 30.1672 32.2320 34.4039 36.5608 38.5537 40.4127 42.1331 HT: Tables 2.1, 3.1, 7.1 estimated

AP Debt Held by the Public 30.1672 32.2325 34.2565 36.2541 38.1388 39.9435 41.6491 43.3608 45.1980 46.9057 48.4489 50.1318 AP: Tables 11-1, 12-1, 12-4 estimated

HT Gross Federal Debt 37.3750 39.4397 41.6116 43.7686 45.7615 47.6205 49.3409 HT: Tables 2.1, 3.1, 7.1 estimated

AP Gross Federal Debt 37.3750 39.4403 41.4643 43.4619 45.3466 47.1513 48.8569 50.5686 52.4058 54.1135 55.6567 57.3396 AP: Tables 11-1, 12-1, 12-4 estimated

AP Debt Held by the Public (% of GDP) 99.4862 100.4879 101.3716 102.0093 102.0518 101.6762 100.9577 100.1520 99.4762 98.3699 96.8223 95.4619 AP: Tables 11-1, 12-1, 12-2. 12.4 estimated

AP Gross Federal Debt (% of GDP) 123.2563 122.9589 122.7009 122.2901 121.3384 120.0237 118.4295 116.8001 115.3398 113.4859 111.2266 109.1871 AP: Tables 11-1, 12-1, 12-2. 12.4 estimated

Gross Domestic Product (GDP) 30.3230 32.0760 33.7930 35.5400 37.3720 39.2850 41.2540 43.2950 45.4360 47.6830 50.0390 52.5150 AP: Table 12-2, page 134

HT Outlays - AP Outlays 0.0001 -0.0006 0.1479 0.1594 0.1082 0.0543 0.0148

Key:

HT: Historical Tables FY 2027, https://www.govinfo.gov/app/collection/budget/2027/BUDGET-2027-TAB

AP: Analytical Perspectives FY 2027, https://www.govinfo.gov/app/details/BUDGET-2027-PER

Note: The above table can be downloaded from https://www.econdataus.com/bud/budget_numbers1.csv

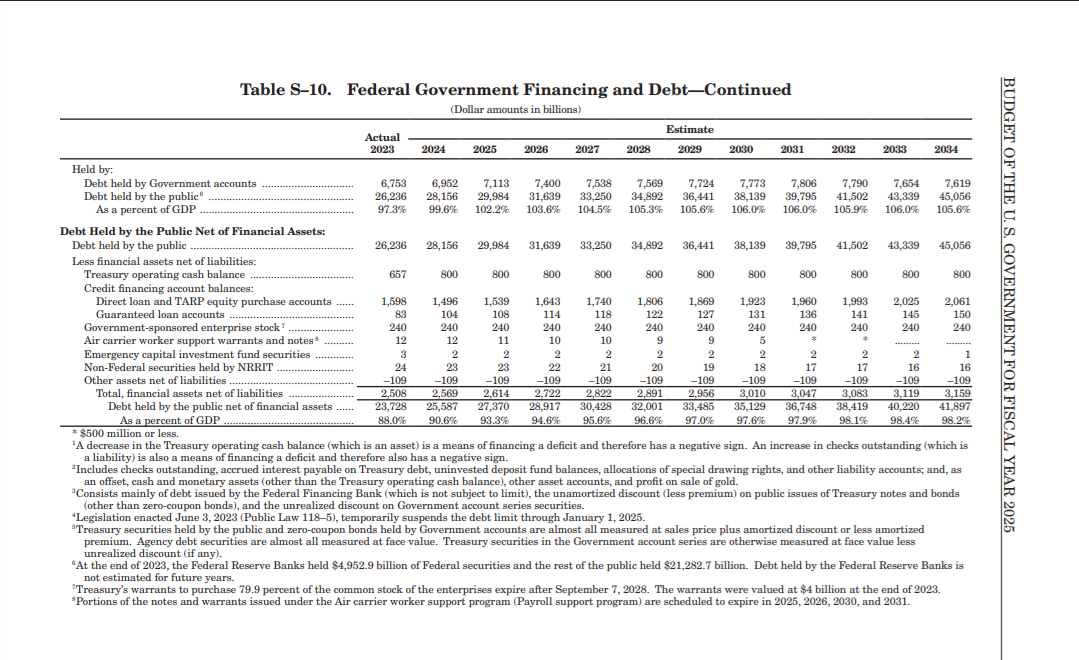

As can be seen, 10 years of projected Receipts and Outlays can be obtained from tables in the Analytical Perspectives. In the Historical Tables, five years of projected Receipts and Outlays can be obtained. From Historical Table 1.1, it can be seen that the Surplus / Deficit (-) is equal to the Receipts minus the Outlays. Despite the fact that only a simple subtraction operation is required, projections of the deficit are not supplied in either the Analytical Perspectives or the Historical Tables. The table above shows this calculation. The calculations show that the deficit is projected to rise from the current $1.77 trillion to $2.02 trillion in 2026 and then decline to $1.68 trillion in 2036. The Historical Tables shows slightly different numbers through 2031, reaching $2.17 trillion in 2027. This difference is due to an difference in projected outlays between the Historical Tables and Analytical Perspectives (shown in the last row).

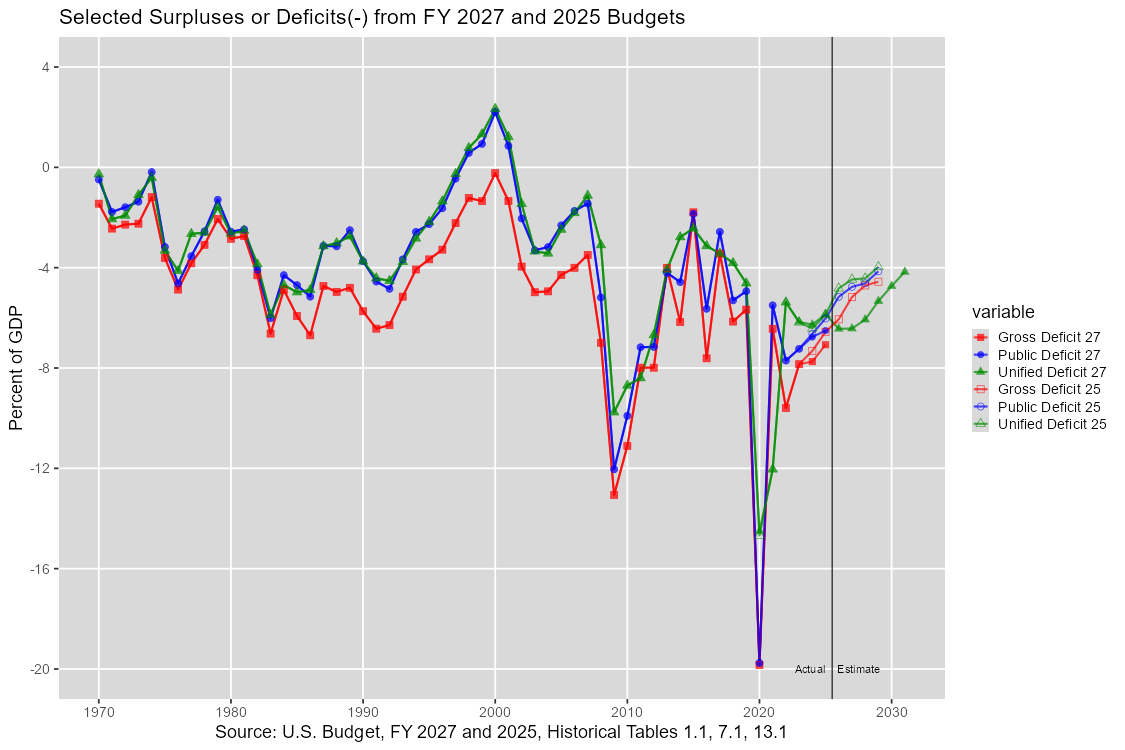

In regards to the debt, the table above shows estimates debt projections that can be obtained from these numbers. The reason why this projections are just estimates can be explained via the following plot:

In the above plot, the green line is the "unified deficit" and the blue line is the change in the debt held by the public (called "public debt" here). As can be seen, they were very nearly equal from 1970 to 2007 but has differed more noticably in years since then. When asked "what is the difference between the unified deficit and the change in the debt held by the public?", following is some of what ChatGPT replied:

They would be identical in a very simple world-but in reality they diverge due to several technical factors:

a) Financing vs. accounting adjustments

The deficit is an accounting measure. Debt change is a cash financing measure.

b) Financial transactions that don't count in the deficit

These increase borrowing but are not counted as spending in the deficit, such as:

Student loan disbursements

Troubled asset purchases (e.g., bank rescues)

Changes in federal credit programs

These can increase debt without increasing the deficit.

Troubled asset purchases did occur following 2007, during the financial crisis. In any case, unified deficits and the change in the public debt appear to be very close on average over time. Still, they are not equal year-to-year and that is why the projections of the Debt Held by the Public are called estimates. The plot above suggests that the change in the Gross Federal Debt tends to be a little larger than these two measures. Hence, the estimate of the Gross Federal Debt is a rougher estimate and is likely a little bit on the low side.

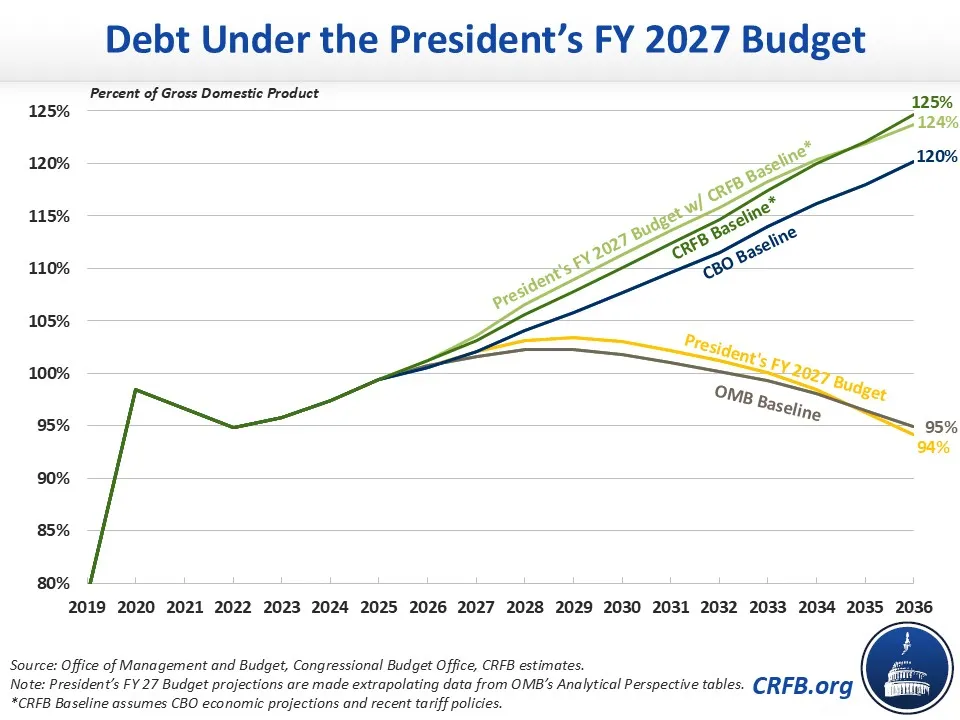

The following chart appears in the prviously mentioned CRFB analysis:

Just before the chart, the analysis states:

Many of the fiscal improvements in the budget arise from the generous assumption of 3% average annual real GDP growth over the next decade. As a result of that growth, the budget's own baseline shows debt peaking at 102% of GDP by FY 2029 and then falling to 95% by 2036.

Those numbers appears to closely match the estimates for "AP Debt Held by the Public (% of GDP)" estimated in the table above.